Payment Options

Alafiora is a private-pay practice by considered design. When you invest directly in your care, you purchase something no insurance panel can authorize and no managed-care framework can replicate: complete confidentiality, unhurried clinical depth, and a record that belongs entirely to you. What you carry into this space will not appear on a benefits statement, inform a future underwriting decision, surface during a life insurance application, or follow you into a security clearance or custody proceeding. It remains, as it should, between us. This page exists because I believe that financial transparency is an act of respect. Read everything. If something remains unclear, bring it to the consultation. We will sort it out together.

Accepted methods

How to Pay

Alafiora accepts a comprehensive and carefully curated range of payment methods so that accessing care does not become an administrative obstacle layered on top of everything else you are already carrying. All fees are collected at the end of each session or charged automatically at the close of each day. Retainer fees are charged separately at the beginning of each month. A minimum of two payment methods is required on file. Should your primary method not process, the second will be used without separate notice. You will know this going in, so there are never surprises.

Personal & standard payments

Debit and credit cards

Contactless payments, including Apple Pay and Google Pay

Cash, personal check, cashier's check, or money order

ACH transfers and bank bill pay arrangements, available by prior arrangement

Health Savings Account (HSA) and Flexible Spending Account (FSA) cards

Health Reimbursement Arrangement (HRA) accounts

CareCredit health financing cards

Employer, institutional & third-party payments

Corporate reimbursement programs and employer-sponsored wellness stipends

Lifestyle Spending Accounts (LSAs)

Select Employee Assistance Programs, by prior written agreement

Union health funds and welfare trusts

Invoicing for professional, forensic, or organizational engagements

“In select cases, family offices, trusts, or corporate entities may arrange direct payment for clinical, concierge, or retainer services. These arrangements require a separate written agreement that clearly protects your confidentiality and confirms that you remain the clinical client regardless of the source of payment. Your privacy is not negotiable, and it will not be compromised by any third-party billing arrangement. If this is relevant to your situation, please raise it during the initial consultation or your first session.”

Out-of-network benefits

Insurance Reimbursement & Superbills

Alafiora does not participate with insurance panels. That is a deliberate and principled decision, not a limitation. It does not, however, mean your insurance cannot contribute to the cost of your care. Many PPO and select other plan types include out-of-network mental health benefits that reimburse a meaningful portion of each session once your deductible is met. I provide a detailed monthly superbill with everything your insurer requires to process your claim: my legal name, NPI, Tax ID, dates and duration of service, CPT codes for each session type, the fee paid, and a diagnosis code where one is clinically indicated and you have provided your informed consent for its inclusion.

Before your first appointment, I encourage you to call the member services number on the back of your insurance card. The questions below are yours to read directly from this page.

A considered script for your insurer

What are my out-of-network mental health benefits?

What is my deductible, and how much of it remains this year?

After my deductible is met, what percentage do you reimburse for out-of-network psychotherapy?

What are your allowed amounts for CPT codes 90791, 90834, and 90837?

Do I need prior authorization to see an out-of-network psychologist?

Are there session limits or any other restrictions I should be aware of?

How do I submit a claim, and what is the deadline for submission?

“I cannot guarantee what your insurer will reimburse, or whether they will reimburse at all. That determination belongs entirely to them. What I can guarantee is that your superbill will be accurate, complete, and submission-ready so that you arrive at that process with everything you need and nothing left to chase.”

Single-case agreements

If your plan cannot provide timely access to an in-network psychologist with my specialization, you may be eligible to request a single-case agreement, sometimes called a gap exception. This is a formal authorization from your insurer to receive out-of-network services at in-network cost-sharing rates, granted because your specific clinical need cannot be adequately met within their network. When requesting one, you may say directly:

Single-case agreement request language

"I require care from a psychologist specializing in complex sexual trauma and compulsive behavior. No suitable in-network provider is available within a reasonable time or distance. I am requesting authorization for an out-of-network single-case agreement with Dr. Esther Lapite-Garrett."

Please note that not every plan grants these requests. Many do, particularly when the clinical rationale is specific and well-articulated. I can provide supporting documentation where it strengthens your case.

Pre-tax options

HSA, FSA & Health Reimbursement Arrangements

If you hold a Health Savings Account or a Flexible Spending Account through your employer, psychotherapy with a licensed psychologist is typically an eligible expense. Paying with pre-tax dollars meaningfully reduces your effective out-of-pocket investment without any additional administrative burden beyond the itemized receipts I provide as a matter of course.

HSA

Funds roll over year to year with no use-it-or-lose-it deadline. Available with most high-deductible health plans. Grows tax-free and can be invested over time.

FSA

Typically operates on an annual cycle. In many cases the full year's election is accessible immediately, even before the account is fully funded. Confirm your plan's specific rules with your benefits administrator.

“I will provide whatever itemized receipts, superbills, or documentation your plan requires. If your employer offers an HRA alongside a high-deductible plan, confirm with HR whether mental health services constitute an eligible expense under your specific arrangement.”

Employer & institutional pathways

Employer Benefits, EAPs & Wellness Stipends

Before assuming your employer benefits are irrelevant to private-pay therapy, it is worth the enquiry. Many clients are genuinely surprised by what their employer already offers and has simply never been asked about. The following questions, directed to your HR department or benefits administrator, are a discerning place to begin.

A considered script for your HR department

"Does our health plan or EAP reimburse out-of-network psychotherapy with a licensed psychologist if I submit a superbill and CPT codes?"

"Is there a mental health stipend, wellness fund, or Lifestyle Spending Account I can apply toward private therapy?"

"Does our plan have a network adequacy exception for specialty care that is not available in-network?"

Additional institutional pathways worth exploring

Employee Assistance Programs that permit out-of-network reimbursement when no in-network provider can meet your specific clinical need

Lifestyle Spending Accounts that classify mental health care as an eligible category

University Student Assistance Programs, health-fee-based reimbursements, or bridge funding for students whose mental health care supports academic functioning

Disability and Accessibility Services offices that subsidize clinically indicated services when tied to documented academic need

VA Community Care referrals for veterans and military families when access standards are unmet or a specialty need cannot be served in-network. Speak directly with your VA provider about a Community Care referral.

Survivor-specific funding

Victim Compensation & Trauma Funds

If you are a survivor of a qualifying crime, state victim compensation programs may cover the cost of your therapy in full or in substantial part. These programs exist precisely so that survivors are not left bearing the financial weight of care they need as a direct consequence of what was done to them. They are underutilized, not because they are inaccessible, but because few people know to ask. You are asking now.

“Most programs require a timely application and documentation. Some states offer alternative processes for survivors who did not file a police report. I can prepare invoices, superbills, and supporting clinical documentation for your claim. If you are working with an attorney on a settlement or restitution matter, it is worth discussing whether therapy costs can be formally included. I will provide whatever documentation your attorney requires.”

Additional pathways for accident and workplace-related care

Auto insurance Med-Pay and Personal Injury Protection policies may cover post-accident therapy. Contact your auto insurer to confirm coverage under your policy.

Worker's compensation may cover therapy related to a qualifying workplace event with a referral from the relevant treating provider.

For clients with active personal injury litigation, please read the lien therapy section below.

Programs and funds to search for in your state

Victim of Crime Compensation Assistance Program (VOCA)

Sexual Assault Assistance Program (SAAP)

Sexual Assault Counseling Fund

Sexual Assault Victim Assistance Fund (SAVAF)

Camaraderie Foundation, for military-connected survivors

SNAP Network survivor resources at snapnetwork.org/victims_of_crime

Faith-based counseling funds and community foundation grants

EEOC settlement funds, where applicable

Worker's compensation, for qualifying workplace incidents

Active litigation

Lien Therapy

For a select number of clients with active personal injury cases or ongoing settlements, Alafiora offers therapy on a lien. This means you receive the care you need and deserve now, and payment is deferred until your case reaches resolution. You should not have to wait for a legal process to conclude before you begin healing. This model exists because that belief has operational consequence.

Lien therapy is offered at a rate modestly above my standard fee to reflect the delay in payment and the administrative responsibilities of the arrangement. It requires a formal lien agreement, signed by you and coordinated with your attorney, who agrees to protect and honor my lien from the settlement proceeds. In the event the settlement fails or falls below what is owed, your attorney assumes responsibility for the outstanding balance as a condition of the agreement.

“Lien therapy is offered selectively and requires a consultation to determine whether it is appropriate for your situation. Please mention active litigation during your consultation so we can assess the arrangement together before any care begins.”

Considered access

Sliding Scale & Scholarship Spots

Alafiora holds a small and carefully considered number of reduced-fee spots, reviewed quarterly. This is not charity. It is a principled part of how I structure a practice that operates at a premium rate: the depth of specialization I offer allows me to designate a defined portion of my capacity for clients whose financial circumstances make full-fee care genuinely inaccessible at this time.

Reduced-fee arrangements are discussed privately during the consultation. I do not require proof of income or financial documentation. I ask that you be honest with me about your situation, and I will be honest with you about what is available and what is not. If a scholarship spot is not currently open, I will tell you directly and help you identify what else might work. There is no shame in this conversation. There is only practicality, and a shared commitment to getting you the care you need.

“I also hold limited pro bono capacity through vetted partnerships with organizations serving underserved survivors. If you are currently receiving services through one of these partner organizations, or believe you may qualify, please mention it during the consultation.”

A thoughtful note

Tax Deductibility

Psychological services may be tax deductible as a medical expense if you itemize your deductions and your total unreimbursed medical expenses exceed 7.5% of your Adjusted Gross Income in a given tax year. This is not tax advice, and I am not a tax professional. What I can offer is a monthly superbill and itemized receipts that give your accountant or financial advisor everything they need to make that determination with accuracy and confidence. If this is relevant to your situation, bring it to whoever prepares your taxes rather than relying on general guidance.

Federal law

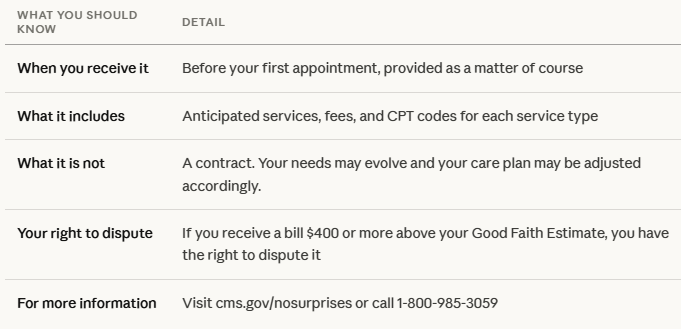

Good Faith Estimate

Under the No Surprises Act, which took effect January 1, 2022, you have the right to receive a Good Faith Estimate of the expected cost of your care before your first appointment, if you are uninsured or if you are not planning to use insurance for our work together. This is not a formality at Alafiora. It is consistent with the transparency and clarity that define every aspect of how this practice operates.

Your Good Faith Estimate will include the services I anticipate providing, the associated fees, and the CPT codes for each. It is not a contract, and it does not prevent your needs from evolving over the course of treatment. What it does is ensure that you are never presented with a bill that does not match what we discussed.

“Please keep a copy of your Good Faith Estimate for your personal records. I will provide one before we begin, without your having to ask.”

When the path is less clear

If None of These Options Apply

There are rare and genuinely difficult situations where none of the pathways above are accessible or available to you. If that is where you are, I want you to know a few things before you conclude that care is out of reach.

Some nonprofit organizations providing survivor services, including rape crisis centers and RAINN-affiliated programs, can engage outside providers as subcontractors under their grant funding through a Memorandum of Understanding. If you are connected to a nonprofit offering supportive services, it is worth asking whether that pathway exists for your situation.

Some local faith communities, mutual aid groups, and community foundations offer short-term financial assistance for healthcare. Asking for what is sometimes called benevolence or emergency assistance for medical care is a legitimate and honored request in many of these spaces.

Network deficiency exceptions exist for situations where your health insurance plan lacks adequate in-network providers for a specific specialty. You may request a gap exception or network adequacy exception, asking your insurer to authorize out-of-network care at in-network rates due to the absence of qualified providers within their network.

If cost is genuinely the only barrier between you and this work, please tell me during the consultation. I will be honest with you about what I can offer. I will also be honest with you if I am not the right fit for where you are financially right now. I would rather guide you toward care that is accessible than have you go without it entirely.

“Please know that I will not accept payment in any context that compromises your safety or my clinical independence. Financial arrangements, regardless of their source or structure, will never influence the care you receive.”